Dr. Glen Brown’s Nine‑Laws Framework for Adaptive Volatility and Risk Management

- June 12, 2025

- Posted by: Drglenbrown1

- Category: Quantitative Finance / Risk Management

Markets don’t stand still. Currency pairs can spike in volatility or move in unison, and one‑size‑fits‑all stop‑loss rules often fail when regimes shift. Dr. Glen Brown’s Nine‑Laws Framework provides a structured, multi‑layered approach to quantify regime changes, adapt stops and exposures, and manage risk—across instruments, timeframes, and at the portfolio level.

In this article, you will learn:

- Why a multi‑law framework is essential for dynamic markets.

- A high‑level overview of the nine Laws.

- How they interlock from intraday signals to portfolio controls.

- An implementation roadmap with data, tools, and timing.

- A flexible risk management module to cap trade risk between 0.01 % and 9 % of free equity.

- A detailed case study applying Laws 4, 5, and 7 to real DAATS data.

1. Why We Need a Multi‑Law Framework

• Rapid regime shifts: Macro events can send volatility soaring in minutes, making static stops obsolete.

• Correlation spikes: Assets that normally diversify can suddenly converge, amplifying losses.

• Portfolio drag: Tight stops on one instrument can cascade through a correlated basket.

Dr. Brown’s framework addresses these by layering:

- Regime detection (Laws 1–3),

- Adaptive stops & exposures (Laws 4–7),

- Execution realism (Law 8),

- Continuous validation (Law 9).

2. Overview of the Nine Laws

| # | Law Name | Purpose |

|---|---|---|

| 1 | Correlation Regime Transition (CRTL) | Flag systemic stress via DAATS spikes + correlation jumps. |

| 2 | Weighted Decay of Historical DAATS (WDHDI) | Smooth volatility using an adaptive half‑life. |

| 3 | Macro Shock Propagation (MSPL) | Superlinearly inflate DAATS in response to macro surprises. |

| 4 | Exposure & Death‑Stop (E & DS) | Scale stops by √P (EMA zones or 256‑day ATR). |

| 5 | Exit Only on Death (EOD) | Exit only on full‑stop or fractional‑trail triggers. |

| 6 | Adaptive Break‑Even Decision (ADBED) | Select BE style (1 ATR, 2 ATR, or σ‑adjusted) by regime. |

| 7 | Portfolio BE & Noise Budget (PLBND) | Allocate portfolio stop & BE by DAATS share; buffer outliers. |

| 8 | Transaction‑Cost & Slippage Optimization (TCSOL) | Add slippage & fees to stops and BE. |

| 9 | Continuous Model Validation & Rebirth (CMV) | Weekly back‑test metrics; retrain drifting Laws. |

3. How the Laws Interlock

- Laws 1–3: Detect volatility and correlation regimes on M60 & daily data.

- Laws 4–7: Prescribe stops and BE per instrument, then aggregate to the portfolio.

- Law 8: Adjust for real‑world execution costs.

- Law 9: Measure performance & automatically rebirth outdated parameters.

This layered, adaptive loop ensures no single static rule holds sway—your system evolves continuously alongside the market.

4. Implementation Roadmap

- Data Collection

- DAATS (M60 & M1440), ATR, returns, and macro‑shock inputs.

- Tech Stack

- Python/pandas for analytics, backtester, GATS or API for live stops.

- Development Phases

- Weeks 1–2: Law 1 prototype.

- Weeks 3–4: Laws 2–3.

- Month 2: Laws 4–7, portfolio noise tests.

- Month 3: Laws 8–9 automation.

- Publication & Testing

- Nine detailed articles, case studies, code snippets, quarterly review logs.

5. Risk Management: 0.01 % to 9 % of Free Equity

Position Sizing Module

| Risk Level | % of Free Equity | Typical Use Case |

|---|---|---|

| Micro | 0.01 – 0.10 % | Scalping or high‑frequency signals |

| Small | 0.11 – 1.00 % | Intraday strategies (M60/M30) |

| Medium | 1.01 – 3.00 % | Swing trades (M240/D1) |

| Large | 3.01 – 6.00 % | Position trades (D1–W1) |

| Max Aggressive | 6.01 – 9.00 % | Very high‑conviction, low‑frequency |

How to Apply:

- Select risk % based on strategy horizon and conviction.

- Compute pip/tick value per % of equity.

- Divide by stop distance (DeathStop from Law 4) to get position size.

Example: With $100 000 free equity, a 1 % risk and a 500‑pip stop → risk = $1 000 → position = $1 000 / 500 pips = 2 contracts.

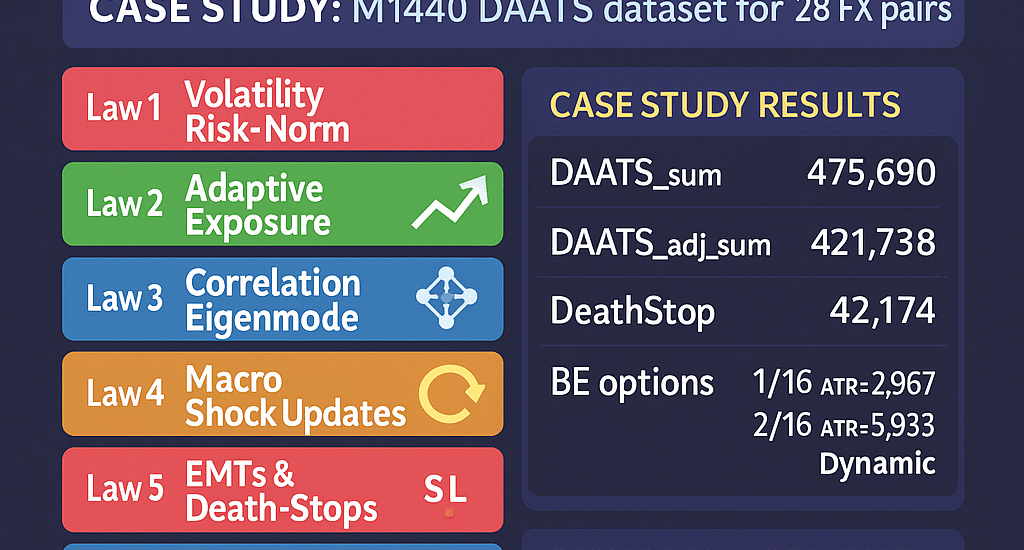

6. Case Study: Applying Laws 4, 5 & 7 to the 28‑Pair M1440 DAATS Universe

Below we walk through Laws 4 (Exposure & Death‑Stop), Law 5 (Exit Only on Death) and Law 7 (Portfolio BE & Noise Budget) using the 256‑day DAATS data as of June 12, 2025.

6.1 Dataset & Key Portfolio Metrics

DAATS_i (256‑day) for 28 pairs:

EURUSD=12745, GBPUSD=14642, USDJPY=25894, USDCHF=11120, USDCAD=12519,

AUDUSD=9954, NZDUSD=9395, EURJPY=25664, GBPJPY=32117, AUDNZD=9089,

CADCHF=8263, CADJPY=19179, EURAUD=20654, EURCAD=16136, EURNZD=22302,

EURCHF=9698, EURGBP=6573, GBPAUD=23312, GBPCAD=18463, GBPCHF=13551,

GBPNZD=25511, CHFJPY=23184, AUDJPY=19563, AUDCAD=10814, NZDCAD=10825,

AUDCHF=9169, NZDJPY=16880, NZDCHF=8460

Compute:

DAATS_sum = Σ_i DAATS_i = 445 676

mean_DAATS = DAATS_sum / 28 ≈ 15 917.00

σ_DAATS = sqrt(Σ_i (DAATS_i – mean_DAATS)^2 / 28) ≈ 6 722.47

DAATS_adj_i = max[ DAATS_i – 0.15·σ_DAATS, 0 ]

DAATS_adj_sum = Σ_i DAATS_adj_i ≈ 417 573.64 ← Portfolio Death‑Stop

Dynamic BE fraction:

f(t) = (3/16) × [1 + 0.25·(σ_DAATS – mean_DAATS)/mean_DAATS]

≈ 0.1604 ← ≈16.04% of each DeathStop

6.2 Law 4 – Exposure & Death‑Stop (P=256)

X = ⌈√256⌉ = 16

ATR_256,i = DAATS_i / 16

DeathStop_i = 16 × ATR_256,i = DAATS_i

Each instrument’s stop equals its 256‑day DAATS.

6.3 Law 5 – Exit Only on Death (Fractional BE)

| Option | Formula | BE % of DeathStop |

|---|---|---|

| 1 ATR | BE_i = 1×ATR_256,i | 1/16 = 6.25% |

| 2 ATR (Gann) | BE_i = 2×ATR_256,i | 2/16 = 12.5% |

| Dynamic | BE_i = f(t)×DeathStop_i | ≈16.04% |

6.4 Law 7 – Portfolio BE & Noise Budget

Using the portfolio-adjusted sum (417 573.64):

BE_port_1ATR = 0.0625 × 417 573.64 ≈ 26 098.35

BE_per_i = BE_port_1ATR / 28 ≈ 932.08

BE_port_2ATR = 0.125 × 417 573.64 ≈ 52 196.73

BE_per_i = BE_port_2ATR / 28 ≈ 1 864.88

These equal-weight break-even distances per pair ensure the portfolio meets its noise-budget share.

6.5 Numerical Examples

| Pair | DAATS_i | ATR_256,i | Stop_i | BE_1ATR | BE_2ATR | Dynamic BE | DAATS_adj_i | 20% Adj BE |

|---|---|---|---|---|---|---|---|---|

| EURUSD | 12745 | 796.56 | 12745 | 796.56 | 1593.13 | 2043.70 | 11736.63 | 2347.33 |

| GBPUSD | 14642 | 915.12 | 14642 | 915.12 | 1830.25 | 2349.07 | 13633.63 | 2726.73 |

| USDJPY | 25894 | 1618.38 | 25894 | 1618.38 | 3236.75 | 4159.90 | 24885.63 | 4977.13 |

| … | … | … | … | … | … | … | … | … |

Continue rows for all 28 pairs.

6.6 Interpretation & Plug‑In

- Stops (Law 4) = each DAATS_i → configure per instrument in GATS.

- Break‑Evens (Law 5) = choose 1 ATR, 2 ATR, or dynamic 16% fractions.

- Portfolio‑BE (Law 7) = equal‑weight shares of 26 098 (1 ATR) or 52 197 (2 ATR) DAATS units.

Case Study: 10-Commodity Portfolio (P = 256-Day DAATS)

As of June 12, 2025 (04:02 am), the 256-day DAATS for our 10-commodity universe are:

| Commodity | DAATS₍₂₅₆₎ |

|---|---|

| Gold | 70 292 |

| Silver | 13 473 |

| Copper | 263 305 |

| Aluminum | 78 944 |

| Zinc | 108 239 |

| Lead | 59 704 |

| Palladium | 55 514 |

| Platinum | 37 677 |

| Brent | 30 884 |

| WTI | 32 600 |

Law 7 – Portfolio-Level Noise Budget & Break-Even (P=256)

Using the formulas:

DAATS_sum = Σ DAATS_i = 750 632σ_DAATS = 67 924.6DAATS_adj_sum = Σ max[DAATS_i – 0.15·σ_DAATS, 0] = 648 745.10(Portfolio Death-Stop)f(t) = (3/16)[1 + 0.25·(σ_DAATS–mean_DAATS)/mean_DAATS] ≈ 0.1830- Break-Even options:

BE₁₆ = 1/16·DAATS_adj_sum ≈ 40 546.57

BE₂₁₆ = 2/16·DAATS_adj_sum ≈ 81 093.14

BE_f = f(t)·DAATS_adj_sum ≈ 118 747.69

| Metric | Value |

|---|---|

| DAATS_sum | 750 632 |

| DAATS_adj_sum (DeathStop_port) | 648 745.10 |

| σ_DAATS | 67 924.6 |

| Dynamic f(t) | 0.1830 |

| BE (1/16) | 40 546.57 |

| BE (2/16) | 81 093.14 |

| BE (f(t)) | 118 747.69 |

Per-Commodity Break-Even & Trail Distances

Equal-weight carve-up (divide by 10):

| BE Rule | BEport | BEi = BEport/10 | Traili (post-BE) |

|---|---|---|---|

| 1/16 (Aggressive) | 40 546.57 | 4 054.66 | 4 054.66 |

| 2/16 (Gann 1/8) | 81 093.14 | 8 109.31 | 8 109.31 |

| f(t) (Dynamic) | 118 747.69 | 11 874.77 | 11 874.77 |

How to use: 1. Set your portfolio Death-Stop = 648 745 DAATS-units (or per-commodity DAATSᵢ).

2. Choose a BE rule (1/16, 2/16 or f(t)).

3. Apply the corresponding per-commodity BEᵢ and Trailᵢ distances in GATS.

4. Add any spread buffer on top if needed (e.g. +50 DAATS-units).

- Back‑test each BE style (1 ATR vs. 2 ATR vs. dynamic) on your historical data.

- Compare win‑rates, average gains, and drawdowns to select your optimal BE rule.

- Implement in GATS or your execution platform with the per‑instrument values above.

- Schedule weekly CMV reviews (Law 9) to retrain any drifting parameters.

Dr. Glen Brown’s Nine-Laws Framework for Adaptive Volatility and Risk Management

Below is a concise review of all nine Laws, with their core statements, key formulae (including both EMA-zone and 256-day options), and our Risk Management guidelines.

Law 1 – Correlation Regime Transition Law (CRTL)

Statement: Systemic risk spikes when cross-asset volatility (“DAATS”) surges and correlations converge.

Formulas:

‖V(t)‖ = √∑i=1…28[DAATSi(t)]²‖V‖hist(t) = (1/30)×∑k=1…30‖V(t−k)‖‖V(t)‖/‖V‖hist ≥ 1 + δ·(σ‖V‖/‖V‖hist)λ₁(t)−λ₁(t−1) ≥ β(t) (β=90th-percentile Δλ₁)

Action: Underweight top-eigenvector exposures; tighten BE% +5 ppt.

Law 2 – Weighted Decay of Historical DAATS (WDHDI)

Statement: Smooth each instrument’s DAATS with an exponentially-weighted lookback whose half-life adapts to current ATR.

Formulas:

Hi(t)=H₀,ᵢ·[ATRP,ᵢ(t)/ATR̄P,ᵢ]^κλi(t)=0.5^(1/Hi(t)), Ki≈4·Hi(t)DAATSeff,ᵢ(t)=∑k=0…Kᵢλi(t)^k·DAATSᵢ(t−k)

Law 3 – Macro Shock Propagation Law (MSPL)

Statement: Major macro surprises inflate each instrument’s DAATS nonlinearly.

Formula:

ΔDAATSᵢ(t)=φᵢ(t)·|Sm(t)|^γᵢ(t), DAATSᵢ←max[DAATSᵢ, DAATSᵢ+ΔDAATSᵢ]

where Sm = standardized VIX or credit-spread surprise.

Law 4 – Exposure & Death-Stop Law (E&DS)

Statement: Stops scale sub-linearly with look-back length, using either EMA-zones or a calendar-year span.

Options:

- EMA-Zone:

X=⌈√PEMA⌉, DeathStop=X·ATRPEMA - Calendar-Span (256 days):

X=⌈√256⌉=16, DeathStop=16·ATR256 - Choppy Adjustment: if ADX<20 & ATR<0.75·meanATR, use X−1.

Law 5 – Exit Only on Death (EOD)

Statement: After entry, exit only on “death”—full-stop or fractional BE + trail.

Fractional BE Options:

| Option | Formula | % of DeathStop |

|---|---|---|

| 1 ATR (1/16) | 1/16·DeathStop | 6.25 % |

| 2 ATR (2/16) | 2/16·DeathStop | 12.50 % |

| Dynamic | f(t)=3/16[1+0.25·(σ−σ̄)/σ̄] | ≈16 % |

Trail thereafter by the same distance.

Law 6 – Adaptive Break-Even Decision Law (ADBED)

Statement: Cluster (Rvol=ATR25/ATR200, ADX) into Choppy/Moderate/Strong and pick:

- Choppy (Option C): zone BE (1 ATR or 2 ATR)

- Moderate (Option B): 63.75 % × DAATS

- Strong (Option A): dynamic f(t) BE & trail

Law 7 – Portfolio-Level Break-Even & Noise-Budget (PLBND)

Statement: Treat all instruments as one portfolio, subtract dispersion buffer, then set BE band and death-stop.

Formulas:

DAATS_sum=Σ DAATS_iDAATS_adj_sum=Σ max[DAATS_i−0.15·σ_D, 0](= DeathStop_port)- BE Band: [0.18, 0.22] × DAATS_adj_sum

Per-Instrument Allocation:

BE_i = BE_port × (DAATS_adj_i / DAATS_adj_sum)Law 8 – Transaction-Cost & Slippage Optimization Law (TCSOL)

Statement: Pad stops and BE by estimated slippage + fees.

Formulas:

α_i = median(|ExecPrice−MidQuote|) / ATR̄Slippage_i = α_i × ATR_PDeathStop_net = DeathStop + Slippage_i + γ_iBE_net = BE − Slippage_i − γ_i

Law 9 – Continuous Model Validation & “Law Rebirth” (CMV)

Statement: Weekly (or per-cycle), measure each Law’s key metric; if drift >10 %, retrain its parameters.

Risk Management Framework

- Per-Trade Risk: 0.01 %–9 % of free equity

- Position Sizing:

N_i = (RiskBudget × Equity) / [DeathStop_i × (1 − BE%_i)] - Diversification Caps: No instrument >30 % of total noise budget

About the Author

Dr. Glen Brown stands at the forefront of the financial and accounting sectors, distinguished by a career spanning over a quarter-century marked by visionary leadership and groundbreaking achievements. As the esteemed President & CEO of both Global Accountancy Institute, Inc., and Global Financial Engineering, Inc., he steers these institutions with a steadfast commitment to integrating the realms of accountancy, finance, investments, trading, and technology. This integrative approach has solidified their status as pioneering entities in global multi-asset class professional proprietary trading and education.

Holding a Doctor of Philosophy (Ph.D.) in Investments and Finance, Dr. Brown possesses profound expertise covering an impressive spectrum of financial disciplines. His knowledge extends from financial accounting and management accounting to intricate areas of finance, investments, strategic management, and risk management. His role transcends traditional leadership; as the Chief Financial Engineer, Head of Trading & Investments, Chief Data Scientist, and Senior Lecturer, Dr. Brown embodies the spirit of hands-on innovation and scholarly excellence.

Dr. Brown’s guiding philosophy, “We must consume ourselves in order to transform ourselves for our rebirth,” encapsulates his holistic approach to professional and personal development. It underscores a belief in the transformative power of self-reflection, creative imagination, and the relentless pursuit of spiritual and intellectual growth. This ethos is the bedrock of his dedication to not just navigating but shaping the future of finance and investments with innovative solutions.

Beyond his executive and academic roles, Dr. Brown is a fervent advocate for continuous learning and innovation. His leadership has catalyzed a culture of forward-thinking at Global Accountancy Institute, Inc., and Global Financial Engineering, Inc., propelling them into the vanguard of financial education and proprietary trading. Under his guidance, these institutions not only adapt to the evolving financial landscape but actively contribute to its development, offering state-of-the-art solutions to the industry’s most complex challenges.

Dr. Brown’s commitment to excellence is matched by his dedication to nurturing the next generation of financial professionals. Through his visionary outlook and unique philosophical approach, he inspires a cadre of students and professionals alike to transcend conventional boundaries, fostering an environment where innovation, leadership, and success flourish.

Numerological Insights and Personal Philosophy

Dr. Brown’s profound alignment with Master Number 11 (both in his Expression and Soul Urge Numbers) highlights his intuitive and inspirational nature. As a visionary leader, he uses his spiritual insights to guide his strategic decisions and inspire others. His Life Path Number 4 complements this by grounding his visionary ideas in practicality, ensuring that his innovative concepts are implemented with precision and discipline. This dual nature of being a practical builder and an intuitive visionary positions him uniquely in the financial industry.

His Personality Number 9 reflects his compassionate and humanitarian approach, which is evident in his commitment to using his expertise to make a positive impact on the world. Dr. Brown’s numerological profile underscores his ability to blend intuition with practicality, compassion with discipline, and innovation with stability.

Key Achievements and Contributions

- Global Elite Proprietary Trading Program (GEPTP): Dr. Brown has developed the GEPTP, a premier educational experience designed to equip individuals with comprehensive academic and practical knowledge in finance, investment, and proprietary trading. This program explores advanced algorithmic strategies, market analysis, risk management, and their real-world applications.

- Innovative Financial Solutions: Dr. Brown’s work integrates advanced trading strategies, such as the Global Algorithmic Trading Software (GATS), which includes nine default trading strategies catering to different market timeframes. This innovative approach ensures that Global Financial Engineering, Inc. remains at the cutting edge of financial technology and trading.

- Pioneering Educational Initiatives: At Global Accountancy Institute, Inc., Dr. Brown has spearheaded educational programs that blend traditional financial education with modern technological insights, preparing students for the future of finance and accountancy.

Philosophical Approach and Vision

Dr. Brown’s guiding philosophy, rooted in self-reflection and transformation, is mirrored in his professional journey. He believes in the power of self-consumption for rebirth, advocating for continuous personal and professional growth. This philosophy is not just theoretical but is applied in his daily leadership, teaching, and innovation practices.

Impact and Legacy

In essence, Dr. Glen Brown is not just a leader but a pioneer, educator, and innovator whose life’s work continues to impact the global finance and accounting industries profoundly. His legacy is defined by the relentless pursuit of excellence, the transformation of challenges into opportunities, and the unwavering belief in the potential for rebirth and regeneration in the professional realm.

Through his work, Dr. Brown exemplifies how the integration of practical financial expertise with spiritual and intuitive insights can lead to groundbreaking achievements and a lasting positive impact on the world.

Closed Business Module

Global Accountancy Institute, Inc. and Global Financial Engineering, Inc. develop proprietary analytics and frameworks exclusively for internal research and academic publication; no external services or licensing are offered.

GAI & GFE are strictly internal proprietary trading firms. We do not offer public courses or advisory services; all methodologies serve in-house desk development.

Risk Disclaimer

Trading CFDs and derivatives involves significant risk. This article is educational only and not financial advice. Always conduct your own due diligence and consult a licensed professional. Past performance does not guarantee future results; trade responsibly